General equilibrium

01/11/2024 - 01/30/24

Zihan

We have learned about the individual optimization and profit maximazition. In these problems, we typically take some elements as given. For example, in UMP, the prices are given. So, in these cases, we are actually looking for partial equilibrium.

Now, under a simple model, we work on a general equilibrium,

Pure exange economy

We have at least two goods.

For simplicity, we consider a static enviornment, in which transactions will not be repeated.

Agents: (individuals or households), indexed by

Goods: We have

Agents are characterized by

their consumption sets:

their preferences over consumption bundles in

Preferences are represented by utility functions, namely

Utility functions need the utility function to be continuous, increasing, and semi quasi concave. (This one is

Assumption 1)Their endowments:

We assume agents have competitive behavior, they take prices as given. (This means each one agent cannot change the price by himself, but this does not mean the price is exogeneously given).

We also assume agents are able to buy and sell any quantities of good they want, which means no friction

Definition 1. Allocation:

Allocation is a list

We need the allocation to be feasible, which means it cannot exceed the aggregate number of endowments, i.e.

The leading example:

Definition 2. Pareto optimum.

A feasible allocation

Explanation to this defination:

For a feasible allocation

It is Pareto efficient if there exists no other allocation

such that for all consumers , with at least one preference relation strict . The process that an allocation

moves to such that for all consumers , with at least one preference relation strict is called Pareto improvement. In other word, an allocation is Pareto efficient if there is no Pareto improvement.

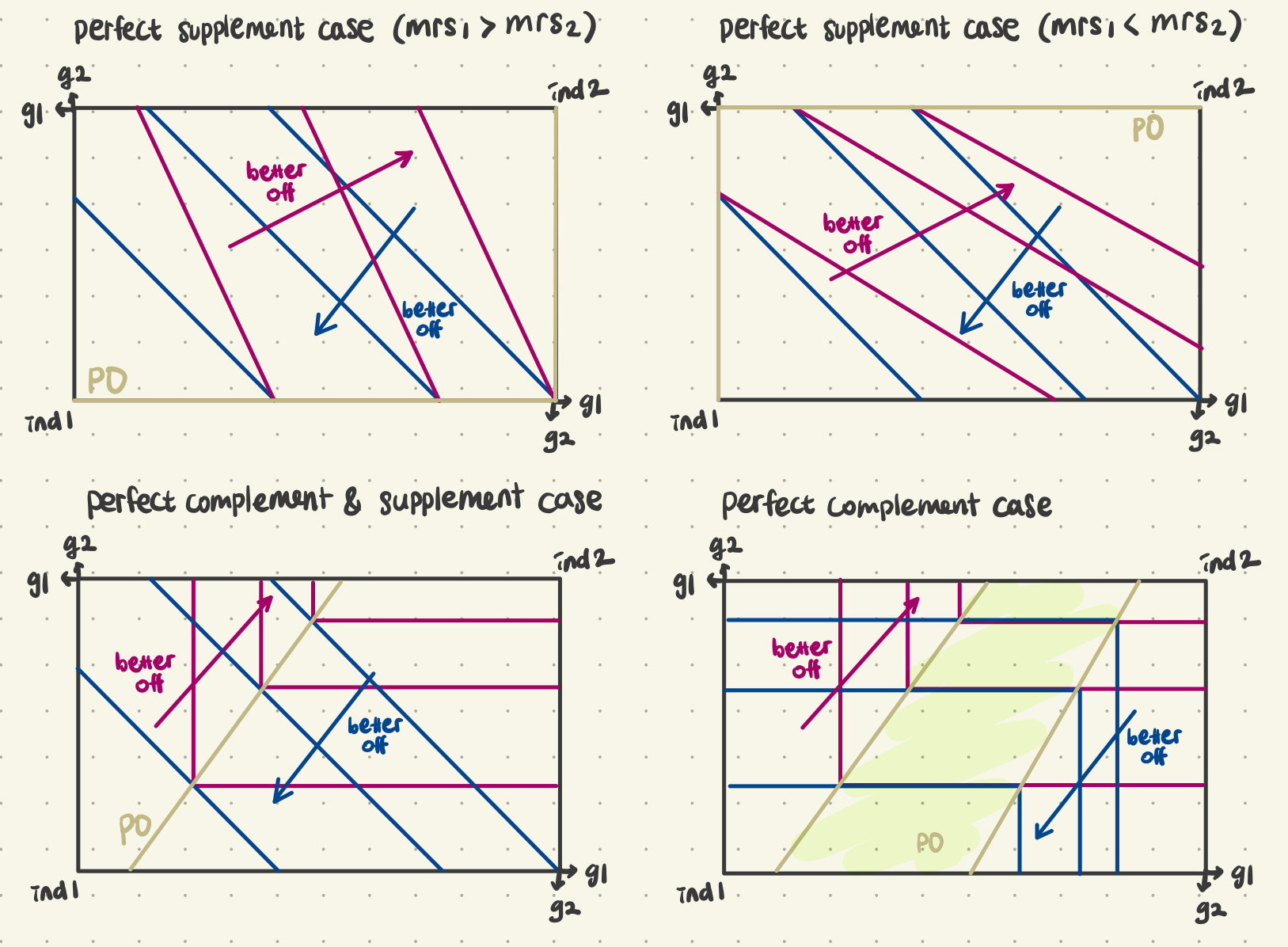

Graphical presentation: Contract curve

All Pareto efficient allocation in Edgeworth box.

Special cases: prefect substitutes; perfect complements

For smooth IC curves, PO allocation one points of tangetly btw IC curves

Problems with PO allocation,

we cannot rank them

we cannot always even rank PO allocation versus non PO allocations

An allocation where one agent gets all the resources is a PO.

Definition3. Competitive

An allocation

Given

market clearing conditions

An example

Definition: Compatitive equilibrium /Walrasian equilibrium

A competitive (Walrasian) equilibrium is a pair

Then we have several famous theorems

[First welfare theorem]: Every competitive allocation is a Pareto Optimum (PO)

[Second welfare theorem]: Any PO allocation can be supported (reached) by with some dedistribution of resources.

Another example

Suppose the utilitty for two consumers are

Endowments:

, How do we derive the competitive equilibrium?

Given

, individual 1 solves By solving this UMP problem,

We can solve the same UMP problem for individual 2 as well,

Then, applying the market clearing condition, what we obtained is,

and,

Two equations above give the same result of price ratio.

subsitute this result back to the demand function, we can get the number of demand for each individual under this endowment.

Here in this example, we did something redundant. Actually we just need one market to be clear, and the other one will be automatically clear as well.

Given endowment

Definition. Feasible allocation and "block"

Let

Under an another allocation, it could be slightly better, i.e.

如果一个allocation

但是即使是Pareto optimum,它这个allocation 仍然可以被其中一个人block。(block by one individual)

Definition. Core

The core of an exchange economy with endowment

推论:Show that

, explain it in own words. Everyone in the "core" is a pareto optimum Suppose there exists a feasible allocation

such that but . Therefore, by definition of Pareto Optimum, there exists a feasible allocation

such that , but some , which has the same meaning of , and for some , . Hence, we know that , which is contradictory to . Hence, whenever

, , which implies .

Recall that we assume agent's utility function satisfies continuity, semi quasi concavity and increasing (strictly increasing), (This is assumption 1).

Each individual is price taker. Given

when

Existance of

Individual

Aggregate excess demand for good

Theorem - Walras law

Let Assumption 1, then

This actually means that the value of aggregate excess demand will always be zero at any set of positive prices.

Proof

By

Assumption 1, It implies budget constraint holds with equality for all, Then,

Thus, if we aggregate over all the individuals it becomes, (note that the order of summation is not important)

Then we obtained what we wanna prove:

An immediate implication of the walres law is that the following:

If given some set of prices that are strictly positive, if

Definition - Walrasian equilibrium

A vector of prices

Walrasian equilibrium 定义的是价格。它使所有商品都不存在超额需求/供给

In this definition, we define equilibrium as price vector. However, the allocation

Theorem - Existance of Walrasian equilibrium,

If each individual's utility function satisfies Assumption 1, and

Definition. [Walrasian allocation] - Given Walrasian equilibrium price

is the Walrasian equilibrium allocation.

From this, we have two observations.

Observation 1letProof

For homework!

Suppose

Observation 2if

This looks quite similar to WARA, if there is some better off utility allocation, it cannot be affordable.

if

Proof

For homework.

We wanna show hat if

Suppose there exists some new allocation such that

Let

Theorem

Let

This implies that every WE alllcation is in the core.

Proof

Proof by contradiction,

On the contrary, there exist

such that and , Since

is Waralsian equailibrium allocation, then from the oberservation 1,, it is a feasible allocation. Then there exists an alternative allocation

and a subset of individuals , such that blocks with . That is

, for all , and for some . We can multiply both sides of

with , then it becomes . And from

Observation 2,for all , and for some , we sum up all individuals in ,

, there is a contradiction.

Definition

Let

Suppose

Note that here each

This allocation

The lagrange function should be like,

FOCs for interior solution give (Here

Example

Two individuals

Say the endowment:

And the utility function

For Agent

, Then,

FOCs:

,

,

This implies,

Substitute with some budget constraints,

, which gives us

describing the PEA.

In Walrasian equilibrium, each individual wants to choose a bundle that maximizes their own utility, She knows nothing about other individuals. By showing WEA is in the core, we have shown that it is possible to believe outcomes in the core without a central planner, which means the market works. that is because

Theorem - First Welfare theorem

If each individual's utility is strictly increasing that every WEA is pareto equilibrium.

Question: Can we consider a WEA as equitable or socially optimal?

It is clear that if an allocation is not pareto efficient, than not socially optimal.

Theorem - Second Welfare theorem

Let assumption 1 for all individuals, let

Proof

Since

is PE, , Since

satisfies Assumption 1, then for all, and , the existence of WEA for and is guaranteed. Let ( )be WEA for economy and , Since under WEA each individual maximizes utilitty given initial endowment, we have,

Since

, we have Since

is PEA, cannot Pareto dominate (That means no such that ), Then

, Suppose

for some , if

then some is strictly increasing, then , contradict! Then

and , Then for

and , for some , (For simplicity let be the only individuals and ), Then by strict quasi concavity, by averaging bundles

and , i can have a new bundle , which gives a higher utility which is a contradiction.

A short summary for welfare theorems

Walrasian equilibrium allocation (WEA)

First welfare theorem: Walrasian Equilibrium

Pareto efficiency

No distortion of price

No externalities

No asymmetric information

No market power

Second welfare theorem:

Any Pareto efficient allocation can result from a Walrasian equilibrium (given that endowments can be redistributed in a lump sum way)

Example

let

Show Edgeworth box, find out PEA, find out WEA, and the prices

This economy in edgeworth box is

For the WEAs, we have to solve the UMP given endowments.

Homework

change the

and , show PEA in this economy

First derive the WEA,

For agent

Then,

The first order conditions are:

Then

, which implies, For agent B, he maximizes

Since the utility function is linear, we have to discuss by case.

If

, then , and In this case, by the market clearing condition,

, we derive , which does not make sense. If

, then , and , In this case, by the market clearing condition,

, . So it could be the WEA. If

, then , but we have under this price, so it could not be a feasible allocation under this price In summary, the WEA is

. Then, the PEA

The Green curve represents the PEA in the edgeworth box. All these POs lie on the edge of the box.

Incorporating Production

We have production in the economy, but let's first consider the most simpliest Rubison economy

There is a firm producing coconut, selling it to Rubison and make profits. Rubison sells labor to the firm.

Say the production function is,

Say Rubinson's utility is,

, where

Rubinson has

Then the budget constraints for Robinson are,

Then, we can set the largrange by,

Here we know that actuall

So

The first-order conditions are,

Then we know the last constraint must be binding, and the solve for the first order conditions, l

Then combine with the budget constraint, we can derive the Rubinson's marshalian demand for coconut and labor,

(Here

Next lets consider the producer's problem. (profit max problem)

Then solve this problem, it gives us firm's demand on labor

And we can derive the profit as well

For completely solving the market equilibrium (general equilibrium), we need to consider the market clearing condition after deriving the partial equilibrium of these two markets.

Labor market clearing: labor demand = labor supply (leisure + labor. = T)

, which gives us

Exams on Feb. 8, TA sessions on Friday.